FREE BETTING INFORMATION

How to effectively manage your betting banks following multiple services

Saturday, 27 January 2024

Share post on

-1617015932.png)

Given the success of our horse racing and sports betting services, the re-subscription rate as you can imagine is very high. In the early days, a reason a couple of members gave for stopping with a service was losses incurred from following other services provided by other tipping companies. We found this curious, as we always figured if each betting service has a separate bank, how can the poor performance of one betting service impact another?

But a couple of recent explanations has led us to understand how this was possible.

Firstly, we must define what the purpose of following multiple betting services is. When it comes to investing by betting on racing or sports, 4 key reasons for following multiple services are as follows:

- More profit (increased turnover)

- Diversification (reducing risk)

- Liquidity limitations (cannot get set for unlimited amounts at acceptable odds)

- Protecting bookie accounts (spreading focus of bets on a wide variety of markets so accounts are not shut down)

The key topic to discuss is regarding diversification, but firstly we will briefly discuss the other three points:

More profit (increased turnover)

This speaks for itself. More betting services means more turnover, which ultimately means more profit, but of course the caveat is the services need to be profitable overall during whatever period you’re assessing.

Liquidity limitations (cannot get set for unlimited amounts at acceptable odds)

With most betting services there is a natural limit to how much you have on their selections.

- Firstly, limits are driven by the fact many bookies will only bet you for a certain amount before the odds are reduced, and taking lower prices impacts your POT%.

- Secondly, some limits are due simply to the fact that one may only be comfortable betting a certain amount before the bet sizes get too large for their comfort zone.

Protecting bookie accounts (spreading focus of bets on a wide variety of markets so accounts are not shut down)

This one is absolutely critical, and in fact in this modern age probably deserves to be number 1. The reality is those who 'specialise' are the first to get restricted or banned by the greedy corporates. The key is to have the bookies and their bots/traders believe you're just another Joe Bloggs getting lucky on the punt.

Must read: How do I avoid getting banned by the bookies

The best way to do this is have a dabble on a bit of everything. I've been advising members for years to place bets across a wide variety of racing and sports options, so you aren't flagged as someone who is betting successfully specialising on a certain niche.

Most smart professionals and punters are happy even just to 'break even' betting on a variety of racing and sports outside their key specialty, in order to keep the bookies off guard.

However, the key topic I want to discuss is DIVERSIFICATION

Diversification is a key element of successful investing, and is defined as the process of allocating capital in a way that reduces the exposure to any one particular asset or risk. A common path towards diversification is to reduce risk or volatility by investing in a variety of assets.

Let’s take a look at how this is achieved in other forms of investment:

Property

In property, investors seek to reduce their risk by investing in a number of properties, as they expect overall that their properties will increase in value over time. However, every market is different, and rises and falls at varying times. As a result, an Australian property investor may, for example, purchase one property in each state of Australia, so he has exposure to each different market and will benefit overall as each state goes through its various growth cycles over time. If one property falls in value, it isn’t disastrous as the investor can simply hold onto that property and still sell or release equity in the other properties as they increase in value.

The biggest risk is if a property investor takes up a loan that is ‘cross-collateralised’ with the other properties. This is where the bank uses the collateral for one loan as collateral for another loan. In simple terms it means the bank considers the whole portfolio together, so if one property loses a significant amount of value, then they can call in the loans on all the properties. Sometimes cross-collateralising can allow someone to obtain a bigger loan, or obtain a lower interest rate. However, it also means one poor investment can ruin an entire portfolio, which is why I personally wouldn’t advise cross-collateralising an investment property portfolio.

Shares

In the share market, investors often buy a variety of different stocks (or a fund) in order to diversify. This means they own a number of stocks, so that if the majority of the stocks go up in value, and a minority go down in value (for relatively equivalent amounts), then overall the portfolio will be in profit.

I’m not a major expert in shares (I stopped trading shares a long time ago when I realised that the profits available through betting far outweighed those available through shares, and for what I consider lower risk), but I tried to think of a situation where investors leveraged or increased their risk, even if ‘diversifying’.

Some investors like more risk for more return, so trade in CFDs. A CFD (Contract for Difference) is a tradable instrument that mirrors the movements of the asset underlying it. It allows for profits or losses to be realized when the underlying asset moves in relation to the position taken, but the actual underlying asset is never owned. However, the kicker is, it is a leveraged derivative. So basically, you can invest 5% of a share, but be exposed to 100% of its value. That’s great if the share goes up, but is disastrous if the share goes down, which is why many people have been bankrupted losing hundreds of thousands of dollars on poor trades through CFDs, and they are banned in many countries.

Why am I telling you all of this and how does it relate to betting?

As you know, we advise you have a 100-unit bank for each individual service.

Well when following multiple services, one must decide how to operate their bank across numerous services, and how much each bank should be worth. There’s a few ways to do this.

Let’s assume someone follows 5 services.

Option A

Run an equal separate bank for each service

- Service A: 100 units (20%)

- Service B: 100 units (20%)

- Service C: 100 units (20%)

- Service D: 100 units (20%)

- Service E: 100 units (20%)

So if you had a $25,000 total bank, each service would have a separate $5,000 bank, betting $50 per unit. This simple & straightforward methodology can be effective.

Option B

Have different banks for each service based on your own assessment of their previous success/performance/profitability, expected variance and number of units they invest per week.

- Service A: 100 units (40%)

- Service B: 100 units (20%)

- Service C: 100 units (20%)

- Service D: 100 units (10%)

- Service E: 100 units (10%)

So you still have a $25,000 total bank, but allocate different amounts of the bank to each service based on your assessment of the above parameters.

- Service A: $10,000 ($100 per unit)

- Service B: $5,000 ($50 per unit)

- Service C: $5,000 ($50 per unit)

- Service D: $2,500 ($25 per unit)

- Service E: $2,500 ($25 per unit)

These banks of course could be variable, and you could re-assess regularly to determine whether a service should have its bank increased or decreased in line with its performance, variance, total monthly units invested and other measurements.

Option C

Have one bank for all services combined

Service A/B/C/D/E: $25,000 ($250 per unit)

This option has the most rapid upside potential, but of course that means it also has the greatest risk attached to it as well.

Your increased investment per unit means that even if all services only break even except one which makes a 100-unit profit in the year, then you will still make $25,000 profit. The issue however, is that you are also equally exposed to the worst performing service. So, if one service loses its bank, you risk losing your entire bank across all of the services you follow.

This is similar to cross-collaterising loans in property, or investing in CFDs (leveraged derivatives) on the stock market. Ultimately it can result in extremely strong profits, but also can result in rapid deterioration of the bank.

This is why we strongly recommend utilising a ROLLING BANK. This means that the value of your unit size should change in line with the changes in your bankroll size.

Say you start with a $10,000 bank, betting $100 per unit. If you have a winning run and your bank increases to $11,000, then one unit should commensurably increase to $110. If you have a losing run and your bank drops to $9,000, then one unit should reduce to $90.

Taking this action reduces your losses during a downturn period, which is absolutely critical. It drastically reduces the risk of wiping out your bank during a losing run. This method also allows you to maximise your profits during a winning period, which allows you to bet more and follow an exponential growth in profits. Whilst you could argue that reducing your bet size during a losing run costs you profit when the inevitable good run comes along, reducing your bet size protects your bank from a losing run that could last longer than you’d like, and ensures you stay in the game to benefit from that inevitable good run.

Some professionals and members like to adjust their unit size after every bet. For others, they prefer to do this daily, weekly, monthly or quarterly. Conversely some prefer to do this with each incremental bank jump (e.g. if you have a $10,000 bank you may wish to adjust your unit size after every $1,000 increase or decrease). It does come down to personal preference, but ensuring you take some form of action in this regard is most important.

Remember if we circle back to the reason for following multiple services, there are four key reasons

- More profit (increased turnover)

- Diversification (reducing risk)

- Liquidity limitations (cannot get set for unlimited amounts at acceptable odds)

- Protecting bookie accounts (spreading focus of bets on a wide variety of markets)

Whilst Option C is the best for #1, it is actually worse for #2, #3 and #4. You are not reducing your risk through diversification as much compared to Options A & B, you are not helping to deal with liquidity limitations as your bet sizes are larger, and similarly that is not helping to protect your bookie accounts.

So what do we suggest?

Ultimately which option you choose is up to you, and everyone has different risk/reward tolerances, expectations and investment goals, but our suggestion would be to consider Option B.

Weight your portfolio based on your overall comfort level with each service, based on their previous success/performance/profitability, expected variance and number of units they invest per month.

Diversifying in your betting is very important as it is in all investment types, but as with other investment types like property and shares, it’s important to be diversified to both increase profits AND reduce risk.

As we always state, the key is focusing on the long term. This again is the same with property and stocks. Short-term investment success in any facet is usually rare, fleeting and insignificant, but long-term success can be exceptional when it comes to any form of investing. The key is patience and balancing risk and reward.

In terms of future investment, in most cases how large your bank is currently is irrelevant. What matters is structuring your portfolio to maximise your long-term success.

What about when subscribed to numerous services?

When you begin subscribing to multiple services as an investment portfolio, it’s important to ensure that your portfolio is balanced in a manner that maximises returns whilst reducing risk and volatility.

In the same manner that a share portfolio is diversified to reduce risk, becoming a member of multiple horse racing and sports betting services also diversifies risk. As a result, even though each individual service may recommend a 100-unit betting bank, if you are a member of say 10 services, then a 1000 unit betting bank is too large as your risk is automatically reduced from the portfolio size, and hence having too large a betting bank is reducing the profits you can make.

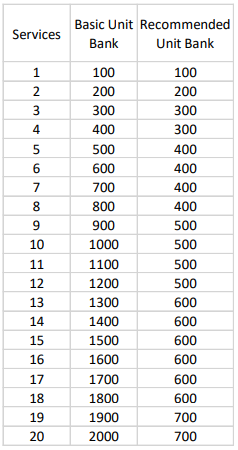

Below is a table showing our recommend unit bank based on the number of individual services you have in your membership portfolio.

Note this assumes each service has a 100-unit recommended betting bank. If a particular service has a larger recommended betting bank then you must adjust the figures below for that.

If you would like further information on bank management relevant to your personal circumstances, please feel free to contact Contact Us

-1609849817.png)

-1609850849.png)